When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

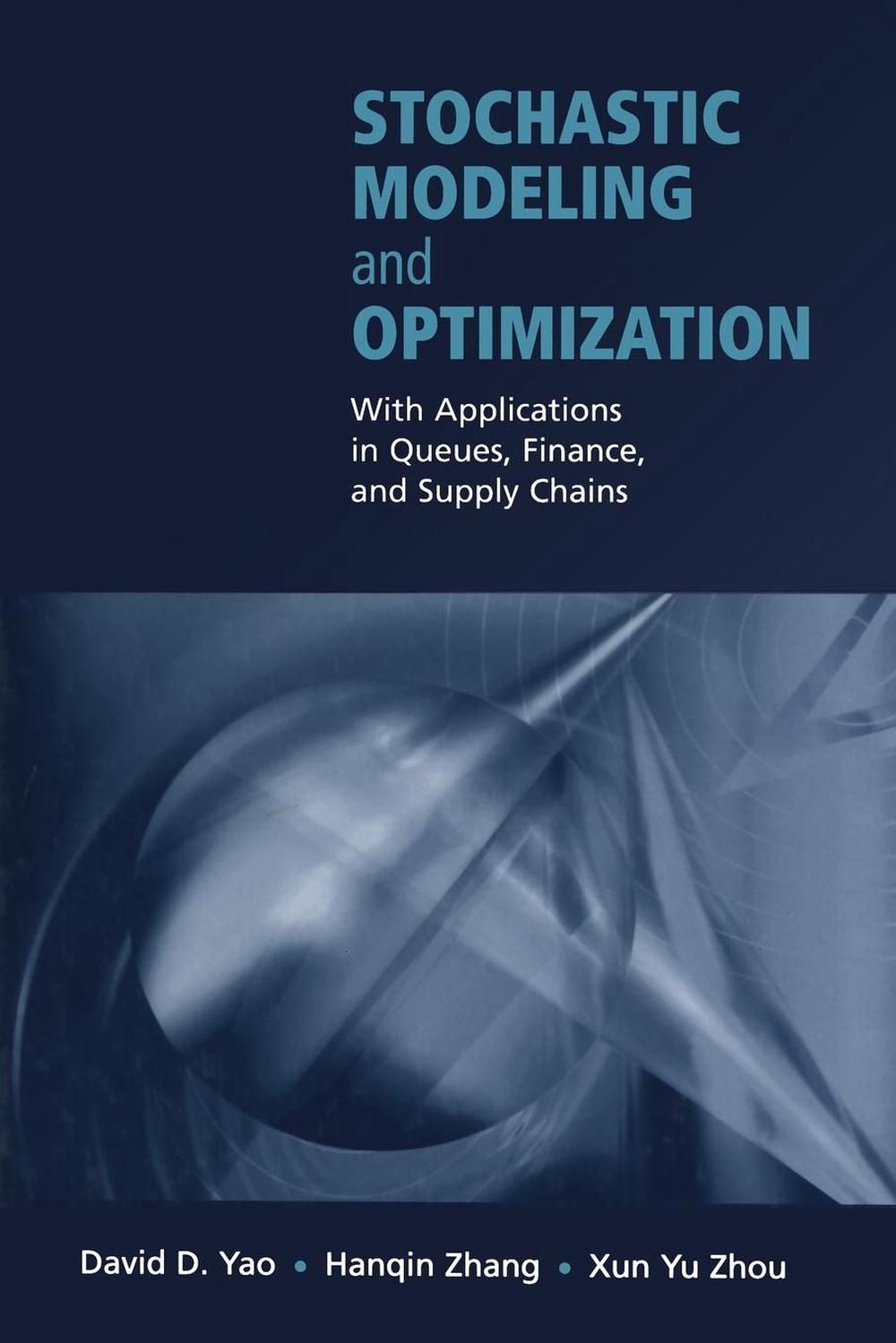

Stochastic Modeling and Optimization: With Applications in Queues, Finance, and

- Item No : 146495821507

- Condition : Brand New

- Brand : No brand Info

- Seller : the_nile

- Current Bid : US $72.97

-

* Item Description

-

The Nile on eBay

Stochastic Modeling and Optimization

by David D. Yao, Hanqin Zhang, Xun Yu Zhou

The first part is a col lection of several basic methodologies: singularly perturbed Markov chains (Chapter 1), and related applications in stochastic optimal control (Chapter 2);

FORMAT

PaperbackLANGUAGE

EnglishCONDITION

Brand New

Publisher Description

The objective of this volume is to highlight through a collection of chap ters some of the recent research works in applied prob ability, specifically stochastic modeling and optimization. The volume is organized loosely into four parts. The first part is a col lection of several basic methodologies: singularly perturbed Markov chains (Chapter 1), and related applications in stochastic optimal control (Chapter 2); stochastic approximation, emphasizing convergence properties (Chapter 3); a performance-potential based approach to Markov decision program ming (Chapter 4); and interior-point techniques (homogeneous self-dual embedding and central path following) applied to stochastic programming (Chapter 5). The three chapters in the second part are concerned with queueing the ory. Chapters 6 and 7 both study processing networks - a general dass of queueing networks - focusing, respectively, on limit theorems in the form of strong approximation, and the issue of stability via connections to re lated fluid models. The subject of Chapter 8 is performance asymptotics via large deviations theory, when the input process to a queueing system exhibits long-range dependence, modeled as fractional Brownian motion.

Notes

This books covers the broad range of research in stochastic models and optimization. Applications presented include networks, financial engineering, production planning, and supply chain management. Each contribution is aimed at graduate students working in operations research, probability, and statistics.

Table of Contents

1 Discrete-time Singularly Perturbed Markov Chains.- 1.1 Singularly Perturbed Markov Chains.- 1.2 Asymptotic Expansions.- 1.3 Occupation Measures.- 1.4 Nonstationary Markov Chains and Applications.- 1.5 Notes and Remarks.- 1.6 References.- 2 Nearly Optimal Controls of Markovian Systems.- 2.1 Singularly Perturbed MDP.- 2.2 Hybrid LQG Control.- 2.3 Conclusions.- 2.4 References.- 3 Stochastic Approximation, with Applications.- 3.1 SA Algorithms.- 3.2 General Convergence Theorems by TS Method.- 3.3 Convergence Theorems Under State-Independent Conditions.- 3.4 Applications.- 3.5 Notes.- 3.6 References.- 4 Performance Potential Based Optimization and MDPs.- 4.1 Sensitivity Analysis and Performance Potentials.- 4.2 Markov Decision Processes.- 4.3 Problems with Discounted Performance Criteria.- 4.4 Single Sample Path Based Implementations.- 4.5 Time Aggregation.- 4.6 Connections to Perturbation Analysis.- 4.7 Application Examples.- 4.8 Notes.- 4.9 References.- 5 An Interior-Point Approach to Multi-Stage Stochastic Programming.- 5.1 Two-Stage Stochastic Linear Programming.- 5.2 A Case Study.- 5.3 Multiple Stage Stochastic Programming.- 5.4 An Interior Point Method.- 5.5 Finding Search Directions.- 5.6 Model Diagnosis.- 5.7 Notes.- 5.8 References.- 6 A Brownian Model of Stochastic Processing Networks.- 6.1 Preliminaries.- 6.2 Stochastic Processing Network Model.- 6.3 Examples of Stochastic Processing Networks.- 6.4 Brownian Model for Stochastic Processing Network.- 6.5 Brownian Approximation via Strong Approximation.- 6.6 Notes.- 6.7 Appendix: Strong Approximation vs. Heavy Traffic Approximation.- 6.8 References.- 7 Stability of General Processing Networks.- 7.1 Motivating Simulations.- 7.2 Open Processing Networks.- 7.3 Network and Fluid Model Equations.- 7.4 Connection betweenArtificial and Standard Fluid Models.- 7.5 Examples of Stable Policies.- 7.6 Extensions.- 7.7 Appendix.- 7.8 Notes.- 7.9 References.- 8 Large Deviations, Long-Range Dependence, and Queues.- 8.1 Fractional Brownian Motion and a Related Filter.- 8.2 Moderate Deviations for Sample-Path Processes.- 8.3 MDP for the Filtered Process.- 8.4 Queueing Applications: The Workload Process.- 8.5 Verifying the Key Assumptions.- 8.6 Notes.- 8.7 References.- 9 Markowitz's World in Continuous Time, and Beyond.- 9.1 The Mean-Variance Portfolio Selection Model.- 9.2 A Stochastic LQ Control Approach.- 9.3 Efficient Frontier: Deterministic Market Parameters.- 9.4 Efficient Frontier: Random Adaptive Market Parameters.- 9.5 Efficient Frontier: Markov-Modulated Market Parameters.- 9.6 Efficient Frontier: No Short Selling.- 9.7 Mean-Variance Hedging.- 9.8 Notes.- 9.9 References.- 10 Variance Minimization in Stochastic Systems.- 10.1 Variance Minimization Problem.- 10.2 General Variance Minimization Problem.- 10.3 Variance Minimization in Dynamic Portfolio Selection.- 10.4 Variance Minimization in Dual Control.- 10.5 Notes.- 10.6 References.- 11 A Markov Chain Method for Pricing Contingent Claims.- 11.1 The Markov Chain Pricing Method.- 11.2 The Black-Scholes (1973) Pricing Model.- 11.3 The GARCH Pricing Model.- 11.4 Valuing Exotic Options.- 11.5 Appendix: The Conditional Expected Value of hT* and hT*2.- 11.6 References.- 12 Stochastic Network Models and Optimization of a Hospital System.- 12.1 A Multi-Site Service Network Model.- 12.2 Patient Flow Management.- 12.3 Capacity Design.- 12.4 Switching Costs and Quality of Service.- 12.5 Insights and Future Research Directions.- 12.6 Notes.- 12.7 References.- 13 Optimal Airline Booking Control with Cancellations.- 13.1 Preliminaries.- 13.2 TheMinimum Acceptable Fare and Threshold Control.- 13.3 Extensions of the Basic Model.- 13.4 Numerical Experiments.- 13.5 Notes.- 13.6 References.- 14 Information Revision and Decision Making in Supply Chain Management.- 14.1 Industrial Examples.- 14.2 A Multi-Period, Two-Decision Model.- 14.3 A One-Period, Multi-Information Revision Model.- 14.4 Applications.- 14.5 Notes.- 14.6 References.- About the Contributors.

Review

From the reviews:"The Workshop Stochastic Models and Optimization … in May 2001, forms the basis of the present volume. 14 papers from about 60 presentations at the workshop were selected and thoroughly revised making self-contained chapters of a book for a broad audience. It highlighted some recent advances in applied probability achieved mainly by scientists with Chinese background. … The book seems to be very suitable for seminar studies at the graduate level." (Hans-Joachim Girlich, OR News, 25, November 2005)

Promotional

Springer Book Archives

Long Description

The objective of this volume is to highlight through a collection of chap

Review Quote

From the reviews:"The Workshop Stochastic Models and Optimization in May 2001, forms the basis of the present volume. 14 papers from about 60 presentations at the workshop were selected and thoroughly revised making self-contained chapters of a book for a broad audience. It highlighted some recent advances in applied probability achieved mainly by scientists with Chinese background. The book seems to be very suitable for seminar studies at the graduate level." (Hans-Joachim Girlich, OR News, 25, November 2005)

Description for Sales People

This books covers the broad range of research in stochastic models and optimization. Applications presented include networks, financial engineering, production planning, and supply chain management. Each contribution is aimed at graduate students working in operations research, probability, and statistics.

Details

ISBN1441930655Publisher Springer-Verlag New York Inc.Edition 2003rdISBN-10 1441930655ISBN-13 9781441930651Format PaperbackImprint Springer-Verlag New York Inc.Place of Publication New York, NYCountry of Publication United StatesEdited by Xun Yu ZhouDEWEY 510Birth 1950Affiliation Chinese Academy of Sciences, Beijing, ChinaShort Title STOCHASTIC MODELING & OPTIMIZALanguage EnglishMedia BookYear 2011Publication Date 2011-12-12Pages 468Subtitle With Applications in Queues, Finance, and Supply ChainsDOI 10.1007/978-0-387-21757-4AU Release Date 2011-12-12NZ Release Date 2011-12-12US Release Date 2011-12-12UK Release Date 2011-12-12Author Xun Yu ZhouEdition Description Softcover reprint of the original 1st ed. 2003Alternative 9780387955827Audience Professional & VocationalIllustrations XI, 468 p.

-

- The Lost Super Foods

- $ 37.00

- The Self-Sufficient Backyard

- $ 37.00

- A Navy Seals BUG IN GUIDE

- $ 39.00

- Childrens Books Phonics Lot 60

- $ 69.98